The EU is sticking to its plans to unilaterally introduce a “carbon toll”, the so-called “Carbon Border Adjustment Mechanism” (CBAM), even though this is drawing international criticism and putting the EU export industry at risk. Meanwhile, geopolitical tensions are jeopardising global cooperation on mitigating climate change. There are better options for action than introducing the highly controversial CBAM.

The global climate challenge and European leadership

The extraordinarily hot summer in Europe focussed our attention on the urgency of the climate problem. Right now, states are once again striving for solutions at the COP-27 international climate conference in Egypt. But progress is slow. The main emitters of greenhouse gases (GHG) – industrialised and emerging economies alike – fear competitive disadvantages if their industries are faced with higher decarbonisation costs. In its WORLD TRADE REPORT 2022, published at the beginning of COP-27, the World Trade Organisation (WTO) emphasises that some of these countries might therefore try to free-ride on the efforts of the frontrunners. Nevertheless, the EU sees itself at the forefront of international climate policy and has launched its ambitious Fit-for-55 legislative package.

With its envisaged Carbon Border Adjustment Mechanism (CBAM), the EU wants to reduce its carbon footprint and also encourage other countries to step up their climate efforts (see cepStudy of July 2021 and cepPolicyBrief 05/2022). A key provision of the CBAM is that importers will have to buy CBAM certificates at the average price that was payable in the previous year for the allowances of the EU Emissions Trading System (EU-ETS), thereby establishing a “notional ETS”. This will allow the EU to phase-out free allowances, which until now have been granted to EU industries at risk of relocation of their production and the corresponding emissions (“carbon leakage”). The EU Commission considers this to be a better instrument for protecting EU industry than keeping free allowances.

CBAM and geopolitical tensions

Internationally, the EU Commission wants to use the CBAM to induce other countries to introduce carbon pricing. In this way they can avoid their export industries having to pay import levies to the EU. However, this strategy seems to be having only modest and at times questionable success. The response has been limited mainly to plans for the UK, Canada and probably the US to implement their own CBAMs. What is more, it has provoked strong opposition to EU “protectionism” from many key trading partners – including the US whose firms would likely not be exempt from the EU CBAM because the US lacks explicit carbon pricing.

The BRICS countries have called the proposed CBAM discriminatory. Moreover, the EU risks “being accused of economic imperialism” which “could undermine trust” in the EU in international climate negotiations and bilateral relations, notably with developing countries. A major obstacle to international support is that CBAM revenues will flow into the EU budget. Furthermore, the EU currently does not seem to be showing much sensitivity to claims by other countries about their right to industrialise.

In his letter to the COP-26 in Glasgow in November 2021, China’s President Xi Jinping emphasised that: “[…] we need to uphold multilateral consensus. When it comes to global challenges such as climate change, multilateralism is the right prescription.” However, rising geopolitical tensions, not least the war in Ukraine, are threatening to halt international cooperation on climate change mitigation. Russia is no longer seen as a reliable partner by the West and China is now halting climate cooperation with the US after Speaker of the US House of Representatives Nancy Pelosi visited Taiwan.

Against this background, the WTO also warns: “Although border carbon adjustment can, to some degree, help address carbon leakage and limit competitiveness loss, it can also generate trade conflicts and economic losses for countries affected.”

With that in mind, the EU should not exacerbate international tensions by sticking to its CBAM project – a project that, in any case, will not deliver the alleged climate benefits and will harm EU industries.

“The EU should not exacerbate international tensions by sticking to its CBAM project which will not deliver the alleged climate benefits and will harm EU industries.”

CBAM – No help in decarbonising EU production

The CBAM will apply at least to the sectors of iron and steel, aluminium, cement and fertilizers and electricity. These are already subject to the EU-ETS. The limited amount of available emission allowances sets a “cap” on the CO2-emissions of the EU-ETS sectors. Lowering it over time leads to their effective decarbonization.

However, a CBAM will not increase the effectiveness of the EU-ETS, even though all sectors will have to pay for allowances due to the abolition of free allowances, because the effectiveness of the EU-ETS depends only on the decreasing cap. Nor will it change the GHG abatement incentives for hard to decarbonise sectors. They will abate if the ETS-price is higher than marginal abatement costs, otherwise not. Companies that currently receive free allowances have the same incentives because they can sell their allowances and use the proceeds to finance emission reductions if the ETS-price is high enough.

Thus, the CBAM will not make decarbonisation of EU production more effective. At best, it could improve on its efficiency by reducing the demand for some products which would otherwise have to be decarbonised at high cost. This is because a CBAM would allow firms to pass on ETS costs to customers in the EU, as importers would then bear roughly the same carbon costs. There are, however, alternative ways to enable such a pass-through of carbon costs with the aim of reducing demand, which gives rise to the question of whether a CBAM does in fact protect against the relocation of production and emissions (“carbon leakage”)?

CBAM – No solid protection for EU exports

One of the alleged aims of the CBAM is to generate a level playing field between producers in the EU and competitors from third countries. However, the CBAM can only guarantee this – to a certain extent – for EU companies producing for the domestic market vis à vis imports to the EU. Under the CBAM, importing firms face a carbon price that is by and large equivalent to the EU-ETS allowance price, and can thus compete on an equal footing.

EU firms that export to third countries, on the other hand, will be disadvantaged if they no longer receive free allowances as they will have to buy allowances while their competitors on world markets do not face an equivalent carbon price.

Granting free allowances just for exports might result in other severe problems and may do so even without restricting this to the most efficient installations as contained in the European Parliament’s related proposal (see cepPolicyBrief 05/2022). The crucial problem is that restricting free allowances only to exports might be challenged before the WTO as an illegal export subsidy. There is even a risk that a return to the current status quo will become impossible if free allocation is generally found to be incompatible with international trade rules the first time it is brought before the WTO.

CBAM – Not compatible with the EU joining a climate club based on minimum carbon price

Moreover, the CBAM is not apt to foster international cooperation on raising climate ambitions by means of a climate club. A climate club is understood to mean a coalition of countries with high climate protection ambitions, which seeks cooperation and ways to protect itself against carbon leakage

“The Climate Club aims to maintain competitiveness while at the same time ensuring that climate protection provides added value – rather than being a drawback.”

German Chancellor Olaf Scholz, speech at COP-27 in Egypt on 7 November 2022

The CBAM will become problematic if the EU aims in the future for a climate club based on an – explicit or implicit – minimum carbon price and no carbon border adjustment between club members. The EU would encounter serious problems in applying its planned CBAM (see cepStudy 03/2021) – in the form of a “notional ETS” where importers have to buy CBAM allowances at the ETS price:

Firstly, imports from outside the club could be rerouted via club members that only apply the minimum carbon price – circumventing the CBAM. Thus, with an EU-ETS price above the minimum carbon price – which is likely to be the case – EU producers will be at a cost disadvantage. Secondly, it is important to note that this cost disadvantage also applies vis à vis competitors in club member countries because EU producers must pay the full EU-ETS price. Overall, the risk of carbon leakage would increase drastically. Thus, the EU should abandon its current CBAM plans and look for better alternatives.

“The EU should abandon its current CBAM plans and look for better alternatives.”

Alternative 1: Concentrate on carbon leakage protection and cooperation

The easiest way for the EU to proceed would be to concentrate on an adequate carbon leakage protection. In addition, the EU should seek international cooperation without exerting pressure on other countries:

For carbon leakage protection, the EU already has a functioning instrument that only needs to be improved to ensure that EU industry is fully protected: the free allocation of allowances. Instead of misguidedly reducing the amount of free allowances as an “incentive” to decarbonize, the EU should ensure that all emissions up to a benchmark are covered by free allowances. Moreover, it should avoid a rapid run-down of free allowances caused by the decreasing overall cap. This can be done by abolishing the artificial restriction that 57% of all ETS allowances must be auctioned [EU-ETS-Directive 2003/87/EC Art. 10(1)].

For international cooperation, the idea from the German Chancellor, Olaf Scholz, of a “cooperative and open climate club” could serve as a blueprint. It deviates from the theoretical concept of an exclusive club based on a shared ambition expressed through a common (minimum) price for carbon, and border adjustments vis à vis non-members. Instead, the idea primarily aims to identify the common interest of willing countries. This might include solutions for their carbon leakage problems, the establishment of markets for climate friendly products and services as well as the provision of mutual assistance in measuring the carbon content of products. Hence the climate club could also work for countries like the US that do not plan to set an explicit carbon price.

Alternative 2: Form a climate club with a minimum carbon price by applying a climate tax

To allow the EU to safely commit to a climate club based on an explicit or implicit minimum price, if desired, the Centre for European Policy (cep) proposes a “carbon leakage-proof” climate club.

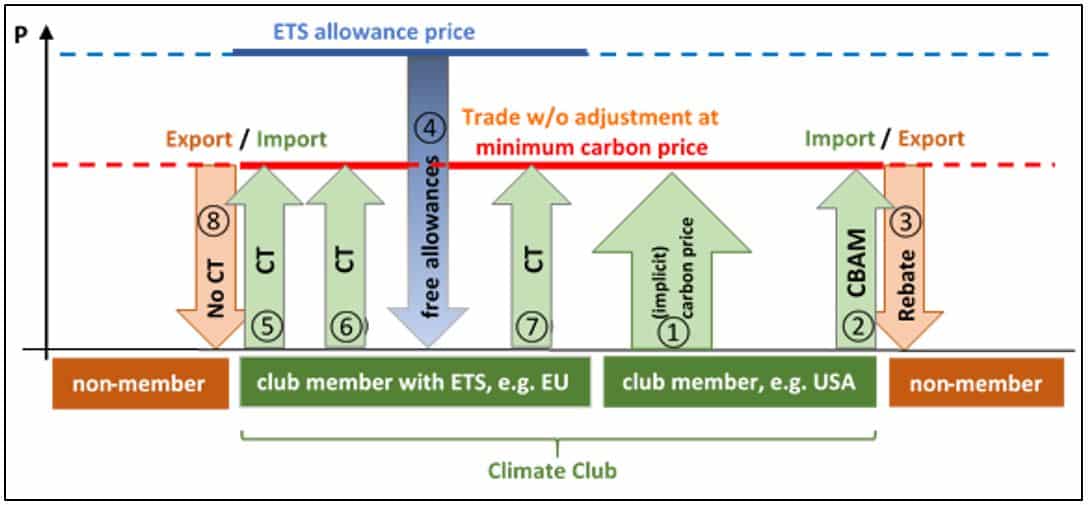

The following diagram illustrates how the elements of the “carbon leakage-proof” climate club would interact:

Member countries without an ETS can use an implicit or explicit carbon price to fulfil the minimum carbon price requirement of the climate club (1). They can apply a CBAM (2) and export rebates (3) to create a level playing field for their industries vis à vis competitors from non-member countries.

For the EU, as in Alternative 1, the free 100% allocation of allowances up to a benchmark would provide the necessary carbon leakage protection (4). However, to establish the minimum price in the EU we refer to the idea of a WTO-compatible, VAT-like Climate Contribution, first proposed by Neuhoff et al. (2016). Since it is a kind of consumption tax based on the carbon content of goods which is imposed both on EU producers and on importers from non-club countries, it is unlikely to give rise to trade conflicts. Our concept uses a slight modification of the Climate Contribution – which we call the Climate Tax. It is only intended as a means to set the minimum carbon price and create level playing fields inside and outside the club. Its aim is not to give carbon emissions a price similar to the ETS price. The latter is not necessary as the ETS price signal is fully functioning for producers falling within the scope of the EU-ETS.

The Climate Tax (CT) is therefore set at the common minimum carbon price of the climate club and applies to imports from outside the club (5), to EU production for the EU market (6) and to EU production for export to other club members (7). Imports from other club members are exempt since they are already “charged” the minimum carbon price there (1). All this creates a level playing field within the club (9). Exports to non-member countries are exempt too, since they are not destined to be “consumed” within the club (8). This, together with the free allocation, achieves a level playing field vis à vis non-member countries.

To sum up, the Climate Tax is imposed on both importers from outside the climate club and on EU firms that produce for customers inside the club. The combination of a sufficient free allocation of ETS allowances and the Climate Tax is not only WTO-compatible but also avoids trade conflicts and is key to the EU safely joining a climate club based on a minimum carbon price. This mechanism is “carbon leakage-proof” inside and outside the club.

“Free allocation of ETS allowances and a Climate tax are the key ingredients for a climate club that is ‘carbon leakage-proof’ inside and outside the club.”

Alternative 3: Use the Climate Contribution to substitute the “notional ETS”

In view of the very advanced CBAM dossier among EU legislators, the most politically plausible alternative might be the proposal from A. Goldthau and K. Neuhoff. They want to replace the “notional ETS” in the CBAM proposal with a Climate Contribution that is likewise set at the average ETS price of the previous year. The Climate Contribution, which is passed on to consumers, creates an incentive to demand fewer carbon-intensive products. Although the ETS would effectively reduce emissions anyway, this demand-reducing effect of the Climate Contribution is seen as crucial especially for basic industries. Unchecked, demand for their products would require a large amount of renewable electricity or green hydrogen to produce them carbon-free. As noted above, the Climate Contribution is WTO-compatible and is not applied to exports. Unlike the “notional ETS”, it can also therefore create a level playing field for EU exports and reduce the risk of trade conflicts.

This alternative can be extended to the case of a climate club with a minimum price. The minimum price could be guaranteed by reducing free allowances for EU producers to countries inside the club in proportion to the price difference between the ETS and the minimum price. This would impose a cost on exporters to club members equal to the minimum price. Exporters to non-club members would be exempt from such a reduction. The carbon price paid in club member countries should, in our view, be deducted from the Climate Contribution to ensure a level playing field in the EU market.

Conclusion

In the face of the energy crisis and geopolitical turbulence, it is now high time for EU legislators to abandon the CBAM project of a “notional ETS” in the ongoing trilogue negotiations. This is crucial to avoid trade conflicts and the threat of dismantling carbon leakage protection for exports. All the alternatives proposed here are better suited to this purpose. They are compatible with international cooperation within a climate club and promote cost-efficient and effective decarbonisation of EU industry through effective carbon leakage protection, rather than displacing it.

“It is high time for the EU to abandon the CBAM project of a ‘notional ETS’. Fierce foreign trade conflicts, the stalling of international cooperation and the threat of dismantling carbon leakage protection for exports must be avoided at all costs. All the proposed alternatives are better suited to this purpose.”

Copyright Header Picture: shutterstock

Könnte Sie auch interessieren

Head of VAUDE, Antje von Dewitz: „We have a bloated bureaucracy, but…“

For a long time, European discussions about democratic backsliding and…

At the Crossroads: European Green Deal Becomes Clean Industrial Deal

EU Climate Policy and Its Socio-economic Challenges

Der ökologische Fußabdruck digitaler Technologien

Die EU will Digitalisierung und Nachhaltigkeit gleichzeitig vorantreiben. Doch…